Nothing should be surprising at this point in 2020. Still, it was surprising that Swedish oat milk company Oatly raised $200 million at a $2 billion valuation from investors including Blackstone, Oprah Winfrey, and former Starbucks CEO Howard Schultz this week. For this to pay off, Oatly needs to increase distribution and build a differentiated brand. That’s a tall order.

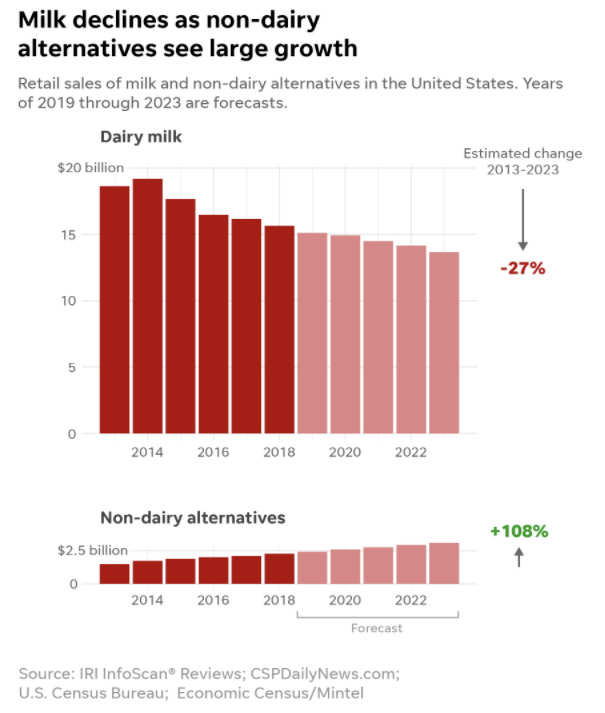

The 30,000 foot view for Oatly is encouraging. In the U.S., milk consumption has been steadily declining for decades while plant-based alternatives like almond, oat, and soy milk have grown:

A growing market is a necessary but not sufficient condition for Oatly to be a successful investment. High growth markets attract competitors. Competition means you need a moat. Total addressable market (TAM) alone won’t save you (more on that here and here). This is where Oatly’s outlook gets fuzzy.

Buy Commodities, Sell Brands

In Berkshire Hathaway's 2011 Shareholder Letter, Warren Buffet wrote that:

“Buy commodities, sell brands” has long been a formula for business success. It has produced enormous and sustained profits for Coca-Cola since 1886 and Wrigley since 1891.

A simple formula, but tough to execute.

While Oatly has nailed the buy commodities part of the equation, the branding aspect is much tougher. When you go to a coffee shop, odds are you order an “oat milk latte” and not an “Oatly latte.” This probably doesn't change.

A quick scan of Amazon shows at least 15 different companies selling oak milk using similar ingredients. While Oatly has patents that could provide some differentiation, I’m skeptical for two reasons. First, most people couldn’t pick Oatly out of a blind taste test. Second, the prevalence of DIY recipes and YouTube videos on homemade oat milk. Oat milk is a commodity.

Gatekeepers & Toll Collectors

Distribution can be a source of competitive advantage for commodity products. As entrepreneur and venture capitalist Peter Thiel has argued:

Superior sales and distribution by itself can create a monopoly, even with no product differentiation.

Because products seldom sell themselves, distribution is critical to scaling a business.

Coca-Cola is the gold standard here. Like Ithaca is Gorges t-shirts or Pittsburgh Steelers jerseys, Coca-Cola is everywhere in the world. Oatly doesn’t need to be as ubiquitous as Coca-Cola to succeed, but it does need to find its way into more and more coffee shops, more grocery stores, and more refrigerators. This won’t be easy. Both offline and online, the company faces powerful gatekeepers and toll collectors.

Let’s start with grocery stores. Like so many industries in the United States, the grocery business is consolidating. Walmart is the nation’s largest grocer, accounting for about 20% of sales for companies like Campbell’s, General Mills, and Kellogg. This gives Walmart tremendous leverage. For example, in 2017 the Wall Street Journal reported that:

America’s packaged-food companies are coming under pressure from retailers who are pushing big brands to lower their prices. On Thursday, Campbell Soup said its sales would suffer this winter because it failed to reach an agreement with a major retailer over promotional pricing and shelf space for its canned soup, its most important product.

The article goes on to say that:

Bob Goldin, a partner at food industry consultancy Pentallect Inc., said the heavy promotional environment is “an intractable problem” in retail. “Constant discounting depresses everyone’s margins; it also trains consumers only to shop on deal,” he said. Campbell, and other brands, can push back, but retailers have the upper hand because they control the shelf space, Mr. Goldin said.

Walmart controls the most grocery shelf space in the U.S. and so it can exert leverage on suppliers. Campbell’s, General Mills, and Kellogg are all more than an order of magnitude larger than Oatly, so Oatly is playing with a weak hand. The company’s trump card is that it’s part of a growing category and retailers like Walmart want to stock products that can drive growth.

Still, Oatly isn’t the only oat milk producer. Walmart may want to devote more shelf space to oat milk, but that doesn’t mean it will devote more shelf space to Oatly. If Oatly wants to be featured over brands like Califia Farms or Silk, it may need to pay for end caps or other shelf-space promotions. No doubt some of the $200 million they just raised will be used for this.

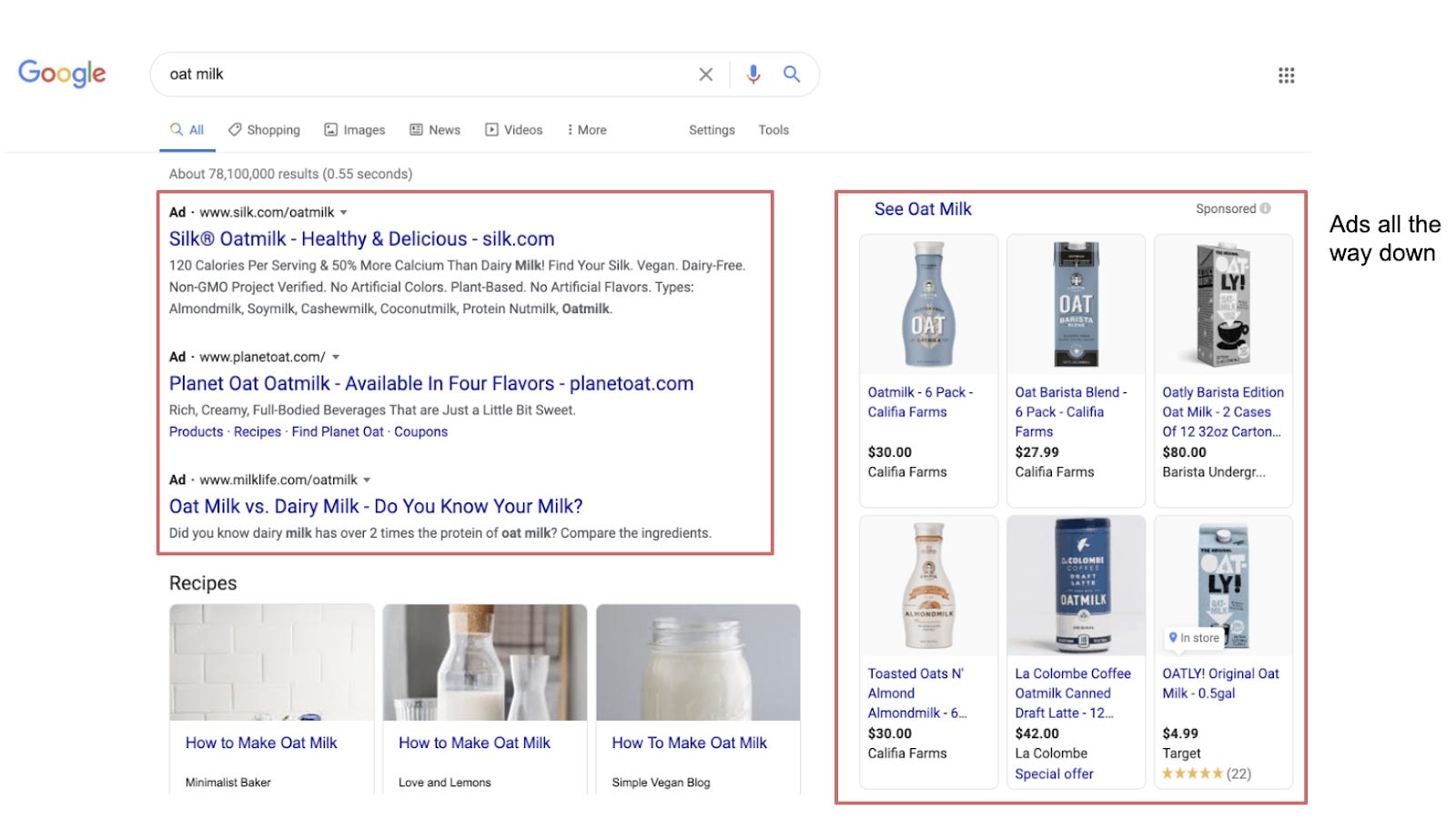

Online distribution channels have their own challenges. In e-commerce shelf space and selection are infinite creating a needle in a haystack problem. The challenge here is discovery. Search “oat milk” on Amazon and here’s what you’ll see:

Lots of ads. Great for Amazon. Not great for Oatly. The company doesn’t fare much better in a branded search for “oatly”:

Google at least has the decency to give Oatly the first result in a branded search. Other queries are less forgiving. Search Google for “oat milk” and its ads all the way down:

Expect Amazon, Facebook, and Google to benefit from Oatly’s $200 million raise.

Offline and online powerful gatekeepers stand in the way of shelf space and discovery. Distribution may end up going to the highest bidder. While Oatly has $200 million of dry powder, competitor Calif Farms raised $225M earlier this year. Other start-ups have war chests as well. Additionally, Oatly has to compete with private labels - an area where Amazon has been very aggressive recently - as well as established global brands like Danone:

Oatly is similar to Casper. It sells a commodity in a box and differentiates with cute branding and light yogababble. As a consumer I want an oat milk latte, not an Oatly latte. From an investment perspective, this might be the wrong lens.

As an acquisition target, Oatly offers an attractive near-term growth profile. In a world of single-digit revenue growth for established companies like Campbell’s, General Mills, and Kellogg, growth is anything but a commodity. An acquisition by a large food player with strong existing distribution is a possibility for Oatly. The company lacks a moat, but growth is a seductive siren song.

👉 If you enjoyed reading this post, feel free to share it with friends!

For more like this once every weekend, consider subscribing👇

The Other Side Of The Story

Here’s a good thread on Oatly’s branding and marketing strategies and how they entered the US. Instead of courting grocery stores and big box retailers, they worked on getting their product to the best coffee shop in each neighborhood:

Before you go

Wanted to flag a podcast from my friend David. It’s niche, but maybe it’s your niche. More below from David:

Not every manga or anime can be the next Dragon Ball Z, One Piece, or Naruto. Shonen Flop is a podcast that takes a look at the series that didn’t make it big and breaks down what went wrong and how they could have turned things around. You can find them on Spotify, iTunes, or their Website; and be sure to follow them on Facebook and Twitter to stay up to date when new episodes come out.