#67 - The Zoom Year

BVP’s 2021 State of the Cloud Report

“Great technology is invisible.” - Steve Jobs

Software became invisible in 2020. As Covid-19 forced work and social life online, software handled more conversations, more work and more transactions. The heavy lifting happened behind the scenes. That text from DoorDash about your dim sum delivery was powered by Twilio. That coffee you ordered online from a small roaster upstate was powered by Shopify.

Once the domain of enterprises, software is everywhere today. As the economy digitizes, it’s permeating industries like construction (Procore) and verticals like auto repair (Shopmonkey) and barbershops (Squire). Zapier, a no-code automation tool, is a prime example of software’s disappearing act. The app lets users automate rote tasks like sending form emails or updating spreadsheets with a few clicks, while software carries water and chops wood in the background.

Bessemer Venture Partners (BVP), a VC firm, has a track record of successful software investing, backing companies like Shopify, Twilio and Wix. Their annual State of the Cloud report provides an overview of software trends. It’s no overstatement when BVP says:

Cloud computing is increasingly consuming software, hardware, and services and is, therefore, the most exciting mega-trend in technology, making it one of the most compelling themes impacting global GDP over the coming years.

Get Rich or Die Trying

2020 was a bumper year for cloud software. Growth rates and access to capital hit all time highs. While software became invisible, industry growth and stock market performance was too large to ignore.

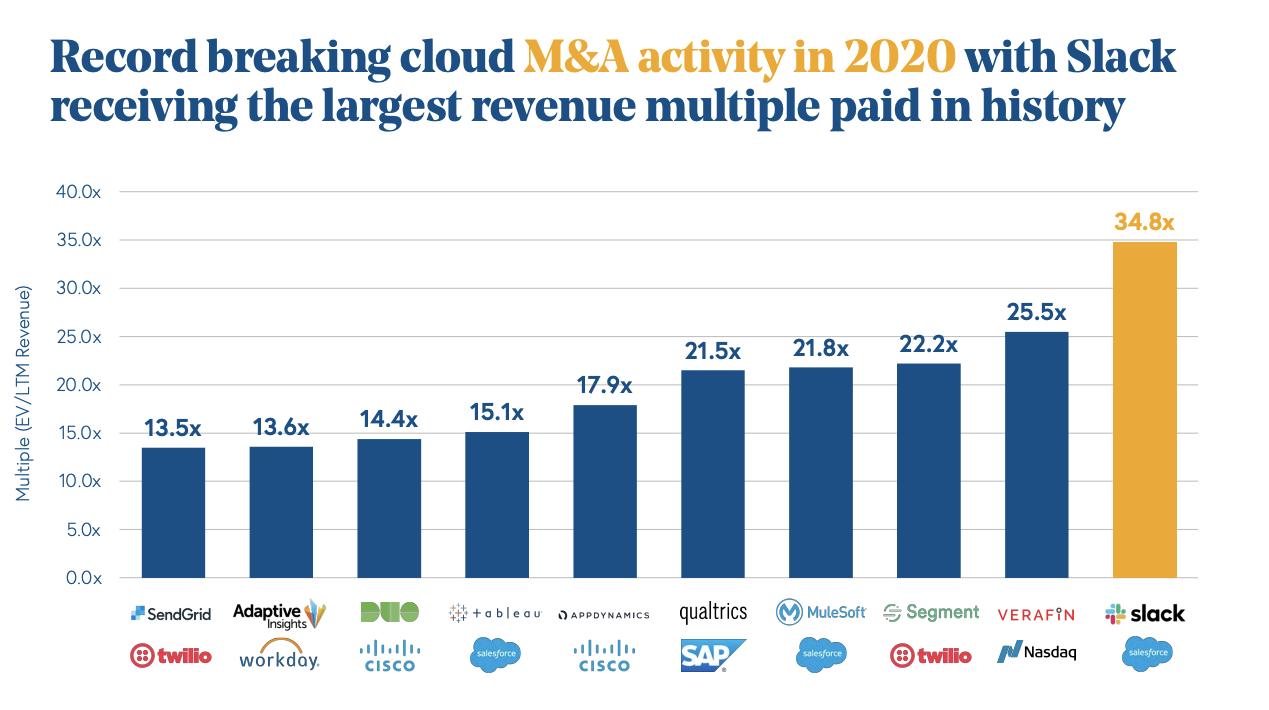

In 2019, no public cloud company was worth more than $200 billion. In 2020, three were: Adobe, PayPal and Salesforce. The combined market cap of public cloud companies topped $1 trillion. Deal activity flourished, with record breaking IPO and M&A activity. Pricing at $34 billion, Snowflake, a cloud-based data-warehousing company, became the largest cloud IPO. The second largest, VMware, went public valued just under $11 billion in 2007. Forebodingly, BVP notes that:

More IPOs last year doubled in value during their opening days than any year since 1999.

Similarly, Salesforce acquired Slack, a chat platform for GIFs (/giphy joke), for a whopping 35x forward revenue multiple. This means that for every $1 in sales that Slack is expected to generate next year, Salesforce paid $35. This is a great outcome for Slack’s early investors. For it to pay off for Salesforce, Slack will need to become very big and very profitable.

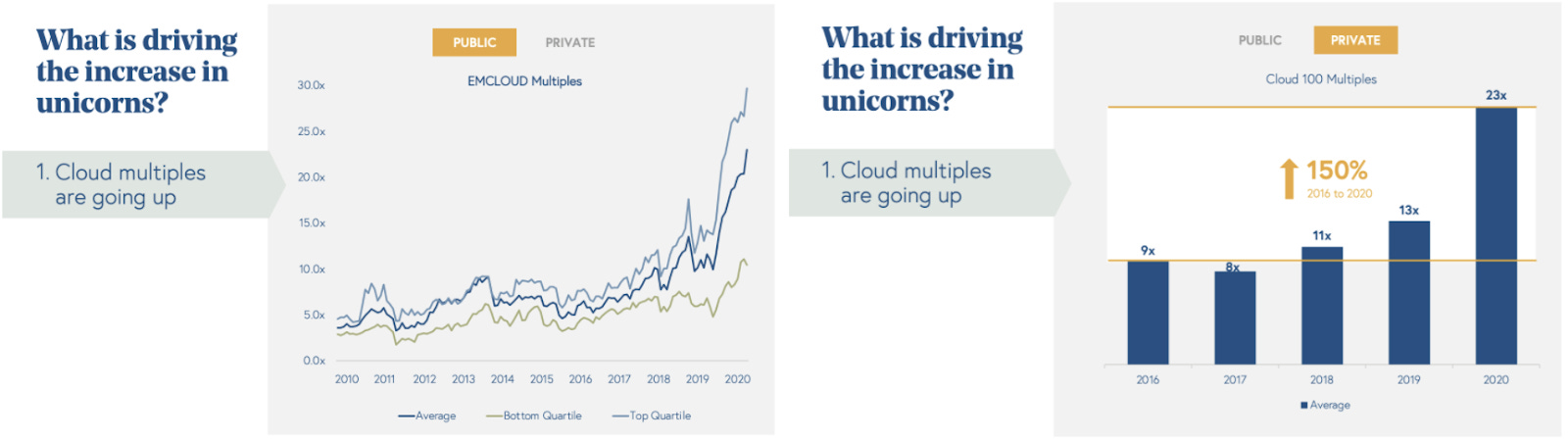

Covid-19 accelerated existing trends, pulling the future forward. This is reflected in valuations of public and private cloud companies. Sales multiples reflect how much an investor is willing to pay today for a $1 of future revenue. A company with healthy growth prospects should fetch a higher multiple than a company with low growth prospects (these companies are likely valued using cash flows or profits). How much higher is the tough part. According to BVP, forward sales multiples for public cloud companies expanded from 5x in 2010 to 20x in 2020 (below left). Private markets have seen multiple expansion as well. The average multiple in BVP’s Cloud 100 index increased over 150% from 9x annual recurring revenue (ARR) in 2016 to 23x ARR in 2020 (below right).

While seemingly precise, multiples exhibit a roller coaster dynamic: expanding when the future looks rosy and contracting when the outlook dims. Multiples are influenced by fundamentals like revenue growth and profitability but also by the availability of capital and psychological factors like fear, greed and FOMO. Determining the right multiple to pay is the central challenge in investing.

Fundamentally, the picture for cloud software is bright. It’s a massive and growing market. The CEOs of Amazon and Microsoft both formerly ran cloud businesses, signifying its importance. Since going public, cloud revenue growth has outpaced Wall Street forecasts (below left). At private cloud companies, revenue growth is accelerating (below right).

The trifecta of high growth rates, expanding multiples, and torrents of capital explain increasing software valuations in 2020. Not mentioned - because who likes a wet blanket? - is the concept of mean reversion, which matters to valuations over the long-haul. Cloud’s expanding TAM justifies higher multiples compared to 2010, but gravity will eventually weigh on 20x revenue multiples.

Get Big or Die Trying

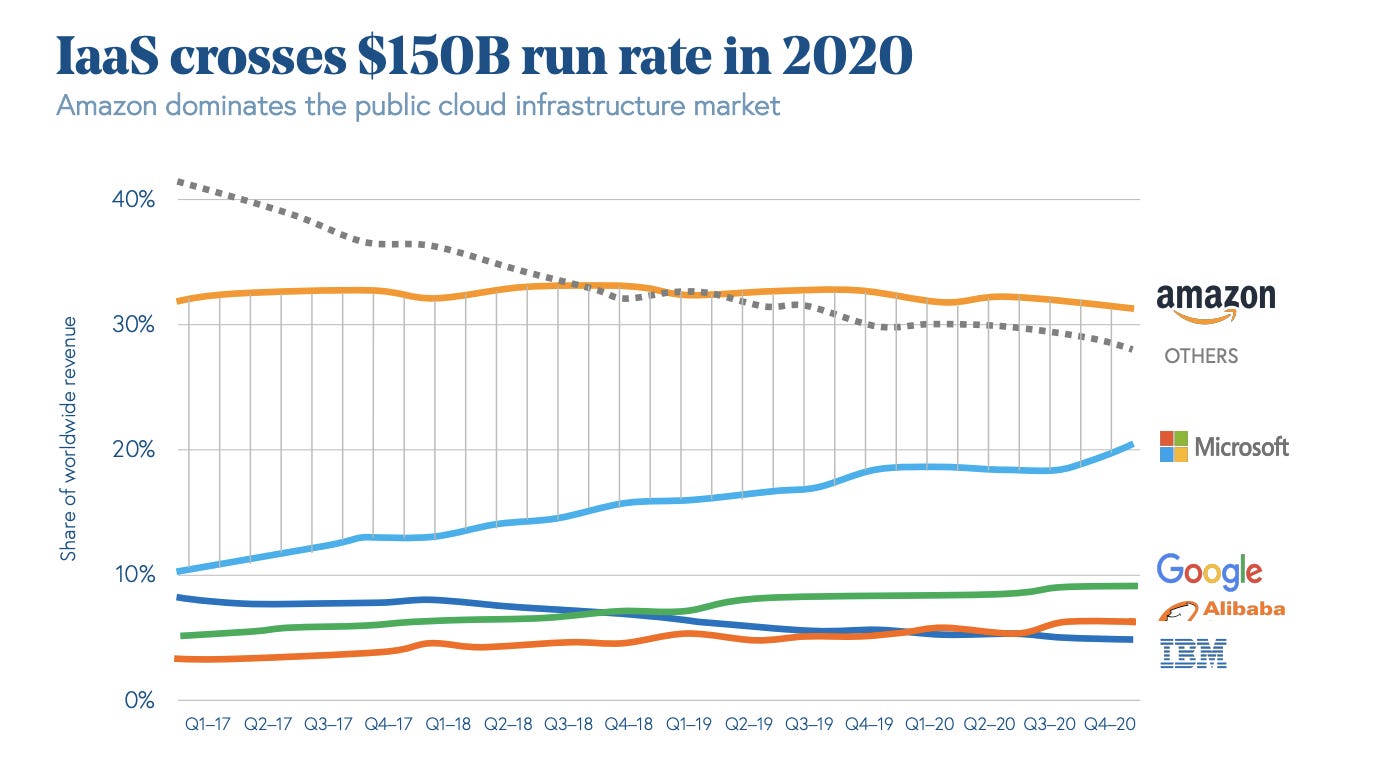

The infrastructure layer (IaaS) is the most mature piece of the cloud ecosystem. As such, it provides a view into how other cloud markets could evolve.

Cloud infrastructure is becoming increasingly top-heavy. Launched in 2006, Amazon Web Services (AWS) is the IaaS leader, controlling about 33% of the market. Microsoft Azure and Google Cloud Platform are smaller than AWS, but growing faster and gaining share. Growth is coming at the expense of smaller players and, of course, IBM.

Increasing concentration isn’t limited to IaaS. It’s a trend playing out across the tech industry broadly. From advertising to video streaming, the top three layers are gobbling up market share at the expense of smaller players, according to an analysis by The Economist. In several markets, the incumbent’s market share has plateaued.

Spoils are disproportionately going to top players. Greater concentration means the ability to pick winners - no easy feat - matters more. Rising valuations increase the cost of picking the wrong horse. In short, lottery tickets are getting more expensive.

In 2020, a record $186 billion was invested in private software companies. A few will grow into market leaders. Many won’t. Like software itself, a few may even disappear.

Want more on BVP?

Here are insights from BVP’s investment memos on LinkedIn, Pinterest and Shopify.

A lot of new readers discover this newsletter from people like you forwarding it to people who they think may like it.

For more like this once a week, consider subscribing 🙏