#128 - Livin’ on a Prayer

Spotify’s 2022 Investor Day

Hi 👋 - Earlier this month, Spotify hosted an investor day defending its business model. The company provided new disclosures around music streaming profitability and podcast performance. Below, an update on Spotify’s podcasting business. Thanks for reading.

🎵If you’re finding this content valuable, consider sharing it with friends or coworkers. 🎵

🎵 For more like this once a week, consider subscribing. 🎵

“When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.” - Warren Buffett

600 Slides Later

Spotify CEO Daniel Ek wants to prove Warren Buffett wrong. Music streaming is a business with a reputation for bad economics. Consequently, Spotify’s business model has a lousy reputation. That’s because three labels dominate supply and capture most of the value. The bear argument on Spotify is that it’s a business with structurally low margins.

Between 2018 and 2021, Spotify’s revenue increased 84% from €5.2 billion to €9.7 billion. Over that timespan, monthly active users (MAU) nearly doubled from 207 million to 406 million. In contrast, gross margins barely budged from 25.7% in 2018 to 26.8% in 2021. Impressive user and revenue growth hasn’t translated into higher margins. To Ek’s chagrin, music streaming’s reputation for bad economics remains intact.

Earlier the month, Spotify attempted to change the narrative at its 2022 investor day. Executives wanted investors to leave with three headlines. First, that Spotify has built a scalable, repeatable machine with a unified consumer experience on the front-end supporting multiple verticals (music, podcasts, audiobooks), monetization models (subscriptions, ads, a la carte), and tech stacks on the back-end. Second, that customer lifetime value (LTV) drives business decisions. Third, that heavy investments in are obfuscating improving profitability. Podcasting plays a central role in all three.

The Case for Podcasts

While Spotify’s moribund stock now trades below its April 2018 direct listing price (a situation that’s becoming increasingly common for tech stocks), business fundamentals have improved since then. For example:

User Growth: MAUs have grown from 207 million in 2018 to 406 million in 2021, a 25% CAGR. Over this period, Spotify has expanded geographically from 65 markets to over 180. This large and growing audience provides built-in distribution for new verticals like podcasts and supports advertising growth.

Churn Reduction: Spotify has improved customer retention while growing its user base. Monthly subscriber churn has decreased 30% over the past four years. For example, premium subscriber churn has fallen from 5.5% in 2017 to 3.9% in Q4 2021. Reducing churn is key to increasing LTVs. The longer a user sticks around, the more opportunities to monetize them. Spotify is a product that hundreds of millions of users love. Scaled, deeply engaged user bases are rare and valuable. However, as the company’s gross margins attest, value capture is more difficult than value creation.

Scaling Advertising: Spotify has grown its ad business to over €1 billion per year, with music accounting for about 85%, but podcasts growing at triple-digit rates. In addition to a large, engaged audience, Spotify has built and acquired ad tech capabilities. Ads will be the dominant form of podcast monetization and the company has shown it can operate a digital advertising business at scale.

Music Gross Margin Expansion: While consolidated gross margins have been stubborn, Spotify’s core music business has been peppier. On a long enough timeline, everyone sells ads, and Spotify is no exception. In 2017, the company launched a confusingly named two-sided marketplace offering promotional tools (read: ads) for artists and record labels. Marketplace revenue grew from €20M in 2018 to €160M in 2021 and is expected to exceed €205M in 2022. This high margin revenue improves Music gross margins.

For its podcasting bets to pay off, Spotify needs to replicate this success on a larger scale. To date, podcast investment exceeds €1 billion, and 2022 will be another heavy investment year. The company needs more podcast listeners, higher podcast monetization, and critically, to improve podcast gross margins.

CFO Paul Vogel’s pitch was that the success of the marketplace strategy is a case study for podcasting1:

We see tremendous upside in Marketplace and anticipate that its financial contribution will continue to grow at a healthy double digit rate in the years ahead. Marketplace is the quintessential example of our approach to capital allocation. There was a significant upfront cost to build and launch these offerings. But, we saw compelling data, which gave us the confidence to double down, and invest aggressively against our goals. And it may have taken time to build up momentum, but our patience and conviction has paid off, and we’re seeing a material benefit from our investment.

Podcast Primitives

Throughout the investor day, executives built an inductive case for podcasting and Spotify’s ability to expand into new verticals like audiobooks (and perhaps education, news, and sports). A number of new disclosures showed that podcasting operational metrics are trending upwards:

Podcasts are Additive: Podcasts are additive to listening hours, increasing time spent on the platform as opposed to cannibalizing music engagement. Customers who listen to podcasts and music steam for twice as many hours as music-only listeners. Spurred by continued MAU growth, overall consumption hours continue making new quarterly records. This is great for Spotify’s ad business as more time spent equals more ad inventory. Additionally, highly engaged users are less prone to churn.

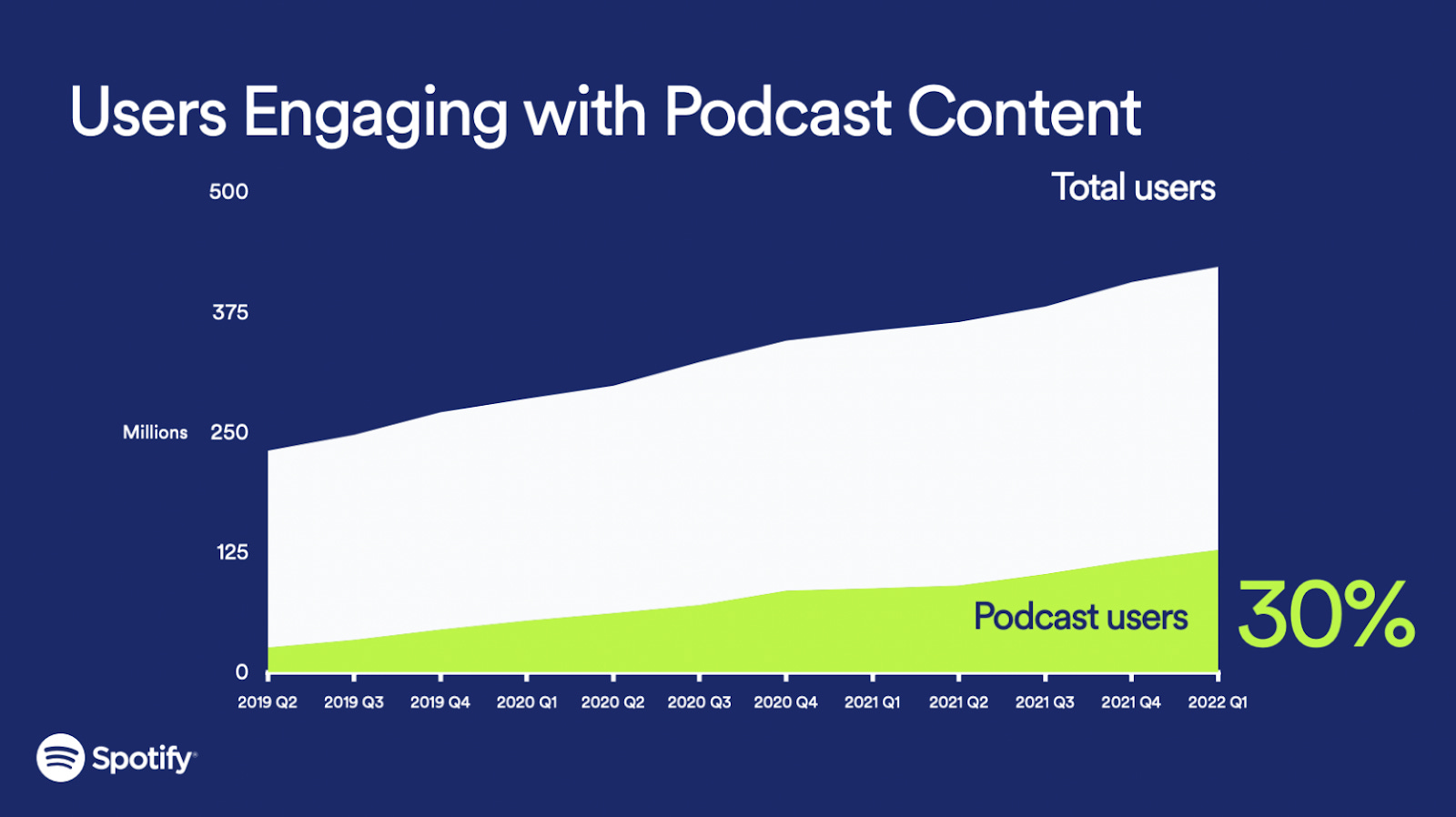

Increasing Podcast Penetration: After a few quarters of playing it coy, Spotify revealed that 30% of MAU listened to podcasts in Q1 2022, up from 25% in Q1 2021 and 19% in Q1 2020.

With this new disclosure, we’ll sadly have to retire this guy for at least a few quarters:

Leveraging Built-in Distribution: Commercializing a new product is easier when you already have direct relationships with hundreds of millions of users. A unified consumer experience - music, podcasts, live audio, and audiobooks all in one app - helps Spotify avoid the cold start problem when entering new verticals. Additionally, Spotify can put its thumb on the scale, nudging users towards podcasts.

Growing Supply: There are over four million podcasts on Spotify. The company’s content strategy is to sign exclusive deals for top shows like Armchair Expert, The Joe Rogan Experience, and Call Her Daddy and supplement these Original & Exclusive (O&E) podcasts with a long-tail of user generated shows. Anchor, a self-serve tool for podcast creators acquired by Spotify in 2019, powers 75% of the podcasts on the platform (though none of the most popular shows). Interestingly, every new Anchor show brings an additional 2.5 MAU to Spotify due to creator promotion, an example of supply begetting demand.

Better Ad Targeting & Measurement: Historically, reliance on RSS feeds meant that the only podcast data available to advertisers was the number of downloads. By moving away from RSS feeds, Spotify is offering advertisers more data and better measurement and targeting options. For example, streaming insertion ads enables podcast ads to be served in real-time. This makes them dynamic. These advertiser-friendly features are available for O&E content and shows hosted on Anchor and Megaphone, which account for about 45% of podcast consumption on the platform. Additionally, more podcasters are making money on Spotify. In May 2020, over 90,000 earned generated some ad revenue (though given power law dynamics, it was likely a pittance for most).

Still the Opening Act

There’s no doubt that Spotify has the raw materials required to build a big podcasting business. A large, engaged audience creates lots of optionality. What’s fuzzier are the returns it'll generate on its investment. The company revealed a number of new podcasting financial metrics, but it will need to do more here given its level of investment:

Revenue: Podcasting revenue grew over 300% y/y in 2021 to approximately €200M, roughly 2% of total revenue. Additionally, substantial growth is expected in 2022 and beyond. Podcast revenue is reported in Spotify’s Ad Supported Revenue, so this is a key item to watch.

Podcast Monetization: Despite 30% penetration, podcasts make up only 7% of total listening hours. Additionally, only 14% of podcast hours streamed are currently monetized. Naturally, monetization lags usage, and usage trends are healthy. For Spotify to generate attractive ROI, both numbers will need to grow substantially. Back of the envelope math suggests that podcasts monetize at a better rate than music: revenue-generating podcasts are 1% of Spotify’s total listening hours (7% of hours x 14% monetization), but 2% of its total revenue 2. In the past, Ek has mentioned that talk could represent about 20% of streaming hours on the platform, consistent with terrestrial radio’s roughly 80% music, 20% talk split. This suggests that podcast listening hour mix could triple through higher penetration and higher engagement, but that’s a far way off.

Gross Margins: While podcasts have the potential to fix Spotify’s gross margin problem, they’re dilutive today due to heavy investment in O&E content. In 2021, podcasts reduced gross margins by €103 million and the 2022 impact is expected to be worse. However, the management expects podcast gross margins to turn positive in 2023 or 2024 and improve from there. Long-term (in roughly 10 years), Spotify sees 40-50% podcasting gross margins compared to negative 57% in 2021. Margin expansion will be driven by operating leverage on the fixed cost of O&E content and growth in higher-margin podcast advertising revenue will drive the margin expansion. For this to happen, the company needs to see additional podcast penetration and engagement growth. Ad Supported gross margins are the most important line on the income statement to track success.

Big Reputation

Ek didn’t upstage Buffett, but on the margin, the case that Spotify has a lousy business model is weaker after the investor day. Spotify provided helpful new disclosure on music streaming profitability and the operational and financial performance of podcasting. Still, there’s a significant gap between “not lousy” and “great” or even “alright.”

In building the case for podcasting, management provided lots of dots, but could have done a better job connecting them all. Their general argument was: we’ve done stuff like this in the past and we can do it again. All of the pieces are there to build a strong podcasting business and I like Spotify’s chances, but as all prospectuses warn, past performance is no guarantee of future results.

🎵If you’re finding this content valuable, consider sharing it with friends or coworkers. 🎵

🎵 For more like this once a week, consider subscribing. 🎵

More Good Reads

The Science of Hitting on Spotify’s analyst day. Sleepwell on Spotify’s entrance into audiobooks. Spotify’s analyst day transcript and podcast. Below the Line on Spotify’s podcast strategy: part one and part two.

Spotify, Spotify 2022 Investor Day Transcript, June 8, 2022.

It’s unclear if this relationship will hold in the future. Today, Spotify is likely monetizing its best content (O&E like The Joe Rogan Experience) in its highest ARPU geographies like the US and Western Europe. Given the size of the business, there’s headroom in all geographies, but at some point, it’ll run into marginal returns.

Great stuff Kevin, and thanks for the shout-out!