#68 - Sweetgreen OS

Restaurant Economics, Tech Debt and the Dangers of DoorDash

Hi 👋 - Scale matters more online than offline. As commerce moves online, industry economics are changing. This week’s post looks at how Sweetgreen, an American salad chain beloved by millennials, is well positioned to benefit from rising e-commerce and food delivery. Thanks for reading. 🥗

Many new readers discover this newsletter when a friend or coworker forwards it to them:

If you aren’t subscribed yet, you can subscribe here:

The first company I worked for used Lotus Notes, an email client developed by Lotus Software in 1989 and seemingly not refreshed since. It also had a custom-built CRM created during the Reagan Administration that was held together with duct tape and bubble gum. If you’ve ever worked for a large company - or used Lotus Notes - then you’ve familiar with tech debt. It’s the notion that past technical decisions weigh down business performance by dampening productivity, limiting capabilities, and increasing frustration. Fixing tech debt requires time, money, and managerial fortitude. Many companies prefer bandaids to surgery.

As e-commerce penetration deepens, technological prowess and access to capital are becoming more important to business success. Sweetgreen, a succulent-filled salad chain with 140 stores and over $450M in annual sales, is a case study on how technology is changing the rules of the restaurant industry. The company prides itself on its direct relationship with farmers, local sourcing, cooking from scratch, and convenience. It also invests heavily in tech and is paranoid of becoming the next Blockbuster, a company that failed because it didn’t adapt.

Restaurant Economics & Dining’s Digital Divide

Traditionally, restaurants are box businesses. Each unit costs a certain amount to build and generates a certain amount of cash flow per year. Investors focus on payback periods, the number of years it takes to return their initial investment, and ROIC. When the model works, you copy and paste the box over and over. No one restaurant is a trophy, but multiply by a hundred or a thousand and you get a big business.

At the unit level, restaurants have high fixed costs. For each dollar of sales, food costs chew up about thirty cents, labor another thirty, rent about ten cents, and discounts and other expenses ten cents or more. World-class restaurant margins are 20%; most operate in the 10-15% range.

Sweetgreen eschews the box model, instead optimizing for market-level economics. The company operates a variety of footprints: flagship locations1, smaller stores, and ghost kitchens exclusively focused on delivery. While flagship stores have lower ROICs, they help with brand building and can boost market returns.

Since launching in 2007, Sweetgreen has operated with an eye on where technology is headed. This tech-forward approach is reflected in the metrics executives focus on. KPIs like average revenue per user (ARPU), order frequency, and cohort data are lifted straight out of an e-commerce S1. According to a 2019 profile in Inc2:

Instead of same-store sales or foot traffic - the traditional retail measuring sticks - Sweetgreen wants to prioritize numbers like active users, lifetime customer value, and, above all, frequency. Order interval, the number of days before a customer orders the same dish again, will become its most critical new measurement.

Without seeing the numbers, this sounds hand wavy and a bit like HBO’s Silicon Valley (regrettably, executives refer to food as “content’). However, Sweetgreen’s financial disclosures suggest the model works: $3 million of revenue per store, industry leading profit margins3, 80% digital orders (up from 50% before Covid-19) and 1.5 million app users who order four times per month.

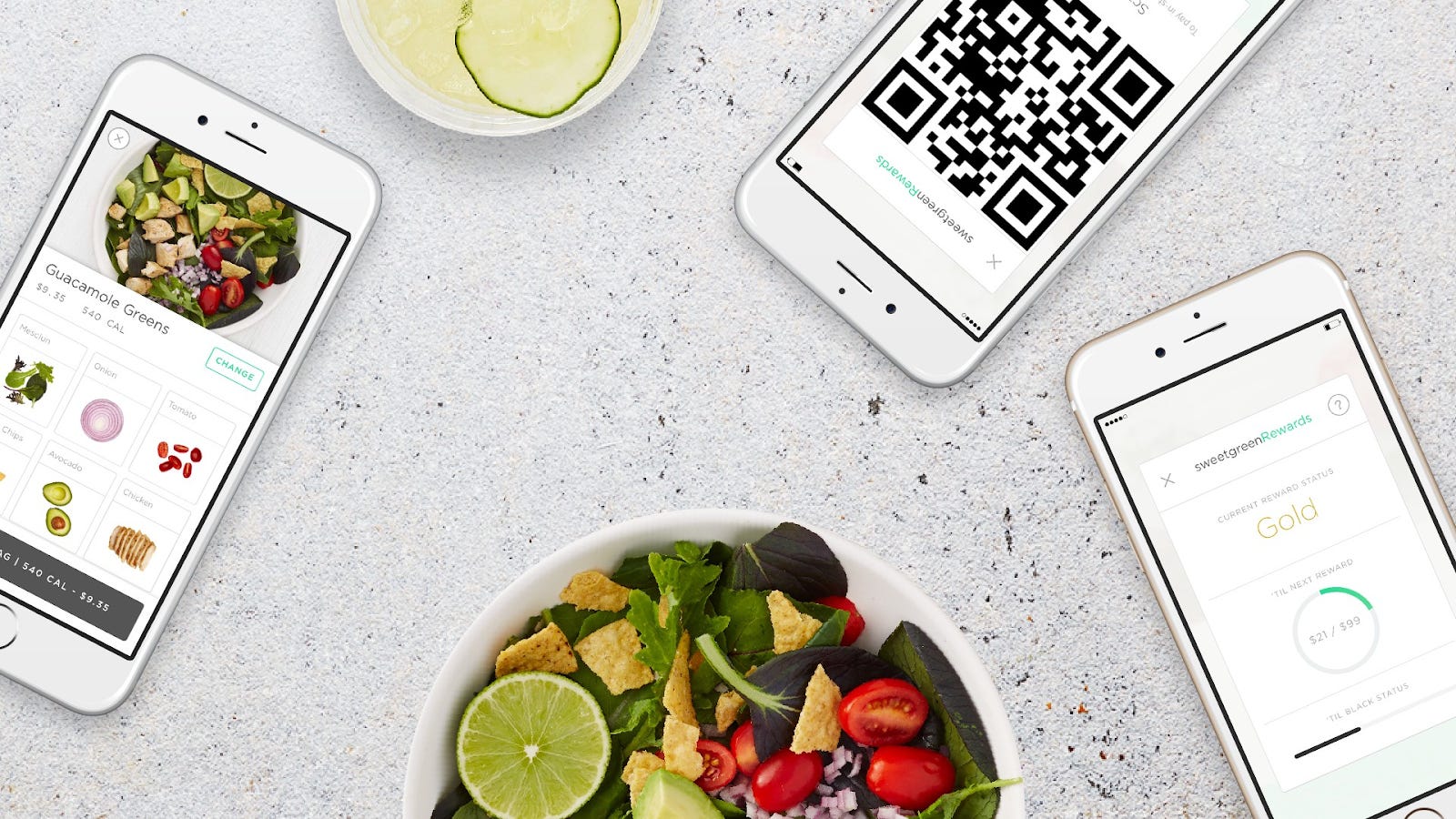

Sweetgreen’s tech-forward approach extends to its operations. It has invested in kitchen automation and supply chain tracking tools, as well as Sweetgreen OS, a restaurant operating system providing demand forecasts, what quantities of food to prepare and when.

Going toe to toe with DoorDash or UberEats on technology isn’t cheap. Sweetgreen has raised $350 million in venture capital allowing it to hire data scientists from Amazon, product managers from Uber, and marketers from Nike. This is a luxury few restaurateurs have.

Don’t Get Blockbustered

For all the tech talk, Sweetgreen is physical business: employees chop kale, roast sweet potatoes, and churn hummus. Tech is an enabler, not the product.

When sales shifted online, Sweetgreen shifted too. In 2013 the company launched its app and started designing stores to better serve online distribution channels. From its twentieth store onward, new restaurants opened with a back of house production kitchen, in addition to the customer facing one. Production lines are more condensed and efficient and fulfill delivery and online pick-up orders. Some restaurants have four or five. Because the future is unknowable and retrofitting restaurants is hard, the company designed modularity and flexibility into stores. Lastly, Sweetgreen devoted more floor space to shelves for online orders. Mobile ordering, production lines, and quick online pickup translate into higher throughput during peak hours like lunchtime.

The company also introduced Outposts in the summer of 2018. Outposts are like Amazon Lockers, but for salads. They serve high-density apartments, hospitals, and office buildings and allow Sweetgreen to batch orders, the holy grail of food delivery. Outpost customers need to place an order by a cutoff time and Sweetgreen delivers for free. They can be served by ghost kitchens, facilities focused on delivery and located off main commercial drags with cheaper rent. Real estate savings help fund delivery. By January 2020, the company had over 700. If successful, the Outpost strategy could turn delivery, historically a cost center, into a profit pool.

Just Chew It (Or, Own the Demand)

Because of its strong brand and direct-to-consumer (DTC) success4, Nike is Sweetgreen’s role model. Since 2017, Nike has pushed direct sales, both in store and online, and built direct relationships with customers.

Always paranoid of becoming the next Blockbuster, Sweetgreen views delivery marketplaces like DoorDash and UberEats as existential threats. Marketplace commissions run up to 30% in an industry where profit margins are 10-20% before delivery. Additionally, marketplaces threaten becoming an intermediary between restaurants and customers, charging fees, and selling ads. The key question is whether marketplaces drive incremental revenue, which is good for restaurants, or cannibalize existing sales, which is very bad. In a recent podcast5, Sweetgreen’s co-founder and CEO Jonathan Neman makes it clear where he stands:

The question is going to be, how many of those restaurants have direct relationships, versus marketplace relationships? Which is in my opinion, the greatest existential risks facing our industry, reminiscent of...Nike versus Amazon, Disney versus Netflix, Four Seasons versus Expedia. It's a very similar story of whoever owns the customer extracts more value in that value chain. And I think that's been a huge focus for us. It has been for years.

Sweetgreen wants to own the customer and extract the value. Its app, which has 1.5 million users, is the keystone of its efforts on this front. Owning the customer relationship allows personalized content and marketing, provides a direct line of communication, and enables payments and loyalty programs.

To fend off marketplaces, Sweetgreen allocates more capital to building out technology than the typical restaurant, according to Neman:

We have to make sure Sweetgreen is the best place to order Sweetgreen. There is a lot more capital in the Sweetgreen-owned native experiences, as well as driving both exclusive content, personalization, and CRM, performance-based marketing within our own properties, versus allocating that capital on our marketplace.

After months of negotiation, Sweetgreen inked a sweetheart deal with UberEats September in 20196. The company pays a lower commission and initially used Uber’s courier network to deliver orders placed through Sweetgreen’s app. The partnership has since expanded to include ordering on the Uber app with an added delivery fee.

In the future, Sweetgreen expects 50% of orders to be for delivery, compared to 25% in 20187. As food ordering shifts online, economic logic changes. Scale matters more. Companies with strong brands and access to capital can develop apps and have negotiating leverage against delivery marketplaces. Small restaurants aren’t as lucky. Lacking resources to invest in technology and drive direct traffic, they may become more reliant on marketplaces who take a cut of each order and own the customer relationship. As the restaurant industry digitizes, Sweetgreen will be alright. If smaller restaurants don’t adapt, they could end up going the way of Lotus Notes.

For more like this once a week, consider subscribing 🥕🌶 🥒

Have a friend who digs Sweetgreen? Please share this with them! 🥗

Other Great Reads

VC Bill Gurley on online marketing and the dangerous seduction of the lifetime value (LTV) formula. Investor Gavin Baker on why leading omnichannel retailers are the major beneficiaries from Covid-19. Baker makes an interesting point a brick and mortar presence can lower CAC by improving online marketing efficiency. Below the Line on how Peloton and digitization are changing the fitness industry.

Eater, Sweetgreen’s So-Called New ‘3.0’ Location Opens in Manhattan Today, October 28, 2019.

New York Times, In a Burger World, Can Sweetgreen Scale Up?, January 4, 2020.

Founders Field Guide, Jonathan Neman - Building the Modern Restaurant, March 11, 2021.

Restaurant Dive, Sweetgreen strikes exclusive deal with Uber Eats, plans to create its own delivery program, September 28, 2019.

Recode Decode, Why Sweetgreen thinks like a tech company, December 17, 2018.