#166 – A Strong Finish, A Fragile Start

Q4 2024 E-commerce Review

Hi 👋 - After years of turbulence, e-commerce found its footing in late 2024. Market leaders Amazon and Shopify extended their reigns, while smaller players eked out gains through product initiatives. But the road ahead looks bumpier. Rising macro uncertainty, cautious consumers, and shifting competitive dynamics shade the 2025 outlook. The era of easy growth and easy money is over – now comes the hard part. Thanks for reading.

If you’re finding this content valuable, consider sharing it with friends or coworkers. ❤️

For more like this, consider subscribing. ❤️

Q4 Results – Ending 2024 On A High Note

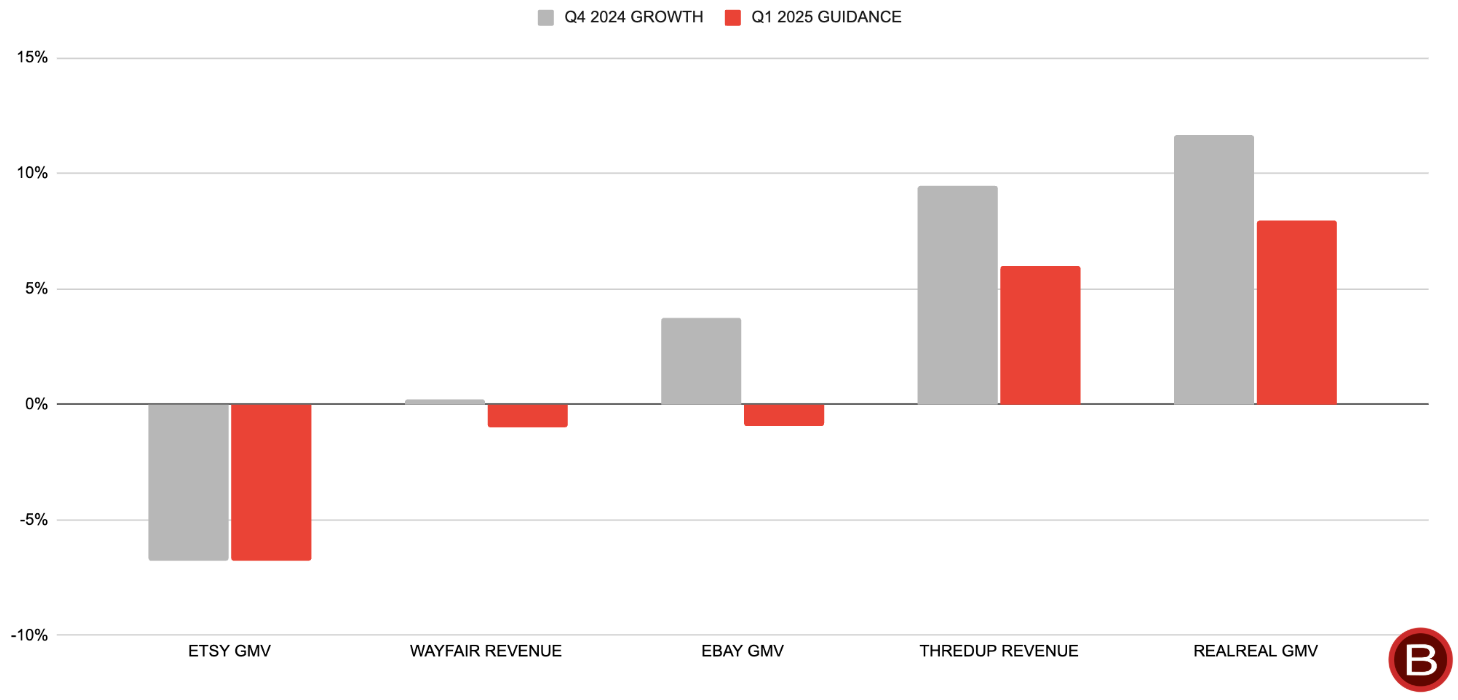

Here’s a sentence I never thought I’d write: eBay outgrew Etsy by ten percentage points. The canonical zero-growth e-commerce business just zoomed the pandemic beauty queen. People make plans and god laughs.

E-commerce closed 2024 on a high note, with most companies seeing accelerated growth in the fourth quarter. The rich-get-richer trend remains intact—Amazon and Shopify continue to outpace the market, consolidating their market dominance.

Amazon is succeeding by nailing the basics: a relentless focus on cost, selection, and delivery speed. Its value proposition is getting sharper. For the second consecutive year, delivery speeds increased while the cost-to-serve decreased on a per unit basis. Providing speedier delivery at lower costs is a moat widening recipe. If e-commerce is a bear, Amazon is a bear tamer.

Shopify is widening its moat too. Its success engine is making it easier for merchants to sell online (and increasingly offline). The combination of healthy same-store-sales, strong merchant acquisition, international expansion, and a growing point-of-sale (brick-and-mortar) presence drove GMV acceleration.

Though dwarfed by Amazon and Shopify, eBay, The RealReal, and ThredUp saw topline gains driven by product initiatives. eBay’s increased investment in focus categories–motor parts, trading cards, and luxury handbags–led to 5% GMV growth1 in these areas, while other categories remained flat. ThredUp and The RealReal benefited from improved supply acquisition strategies.

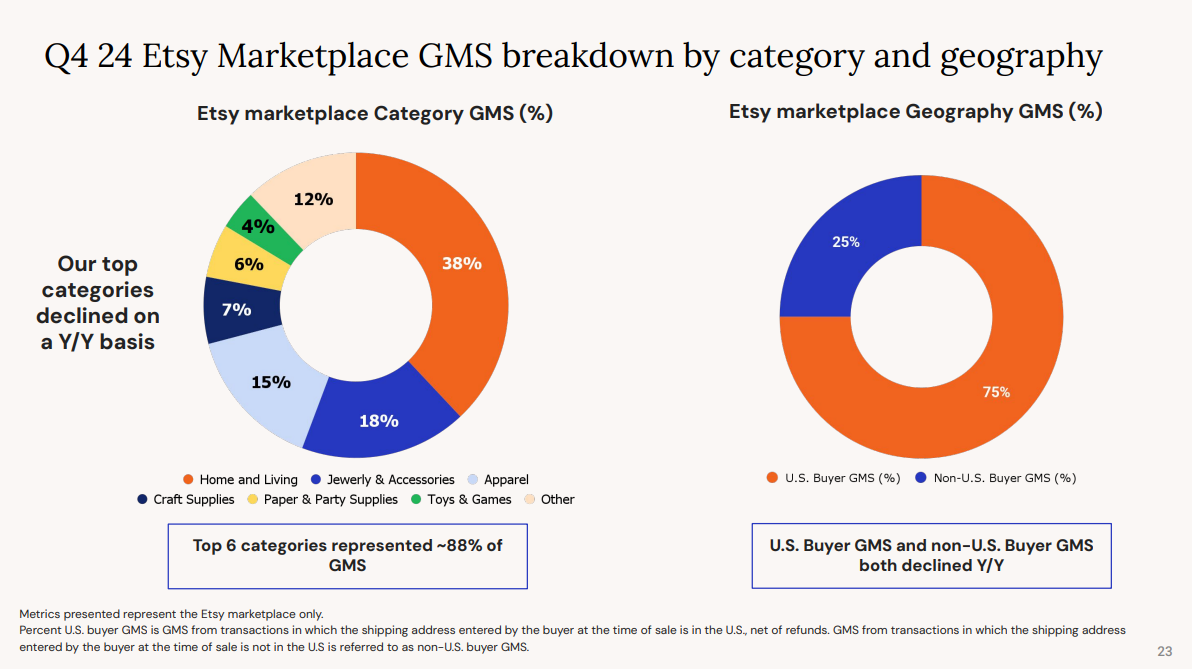

Etsy was an outlier, reporting sequential deterioration. GMV on Etsy.com fell 9%2. Once a pandemic e-commerce darling, it now trails eBay. Heavy exposure to discretionary spending–especially home and living, which accounts for nearly 40% of GMV–is a liability. Yet Wayfair, with 100% exposure to the category, still managed to grow.

Etsy blamed some of this softness to self-inflicted wounds, like shifting product and engineering resources from towards beefier projects like search quality and improving discovery with longer payoffs. It also pointed fingers at the shorter holiday shopping season–an excuse that doesn’t hold water, as every retailer faced the same calendar3. The real problem runs deeper: there’s a kink in Etsy’s growth model.

Q1 Guidance – Growing Caution Amid Rising Uncertainty

If the fourth quarter ended with a bang, the first quarter started with a whimper. Several factors are giving managers the heebie jeebies. Macro uncertainty is rising due to an on-again, off-again, on-again, off-again, on-again, off-again trade war and fading consumer confidence. Adding to the challenge, lapping a Leap Year means on fewer selling day and foreign exchange volatility creates further headwinds for companies with significant non-US dollar revenue streams. Business is never easy, but it’s harder right now.

Wayfair’s CEO, Niraj Shah, underscores the complexities managers face as they plan for 20254:

Our relentless customer and supplier focus has resulted in another quarter of healthy share gains in the face of a category that remains under pressure. I've talked in the past about how the overhang, a depressed housing cycle has had on customers' willingness to spend on their homes. The forward outlook, especially in the core of our business, big and bulky furniture, is as unpredictable as any point in the past four years with uncertainty over the state of inflation, global trade policy and interest rates, among other factors.

The outlook for 2025 points to slower growth, but companies offering full-year guidance—eBay, Shopify, The RealReal, and ThredUp—expect continued expansion. While Etsy didn’t issue formal guidance, it remains optimistic that growth will rebound after the first quarter, driven by easier comps, a shift in focus to more short-term projects, and its 2025 product roadmap.

Shoppers Tighten Their Belts: Value and Convenience Drive Spending

Consistent with the rest of 2024, shoppers want value and remain judicious with discretionary spending. With egg prices where they are, who can blame them?

Price and convenience continue to drive consumer spending, to Amazon’s benefit. Notably, Amazon’s paid unit growth outpaced revenue growth, likely due to efficiency gains that have lowered unit costs and sped up deliveries, boosting orders for essentials and pharmacy items. Meanwhile, cautious consumer sentiment around discretionary spending–highlighted by Etsy and Wayfair–may also be contributing to the trend.

The RealReal is also capitalizing on value-conscious consumers, marketing its discounted second-hand luxury goods effectively and driving accelerated GMV growth. Notably, spending by customers who spent at least $5,000 in 2024 rose 20% year-over-year. Similarly, ThredUp refined its supply strategy to prioritize more desirable and premium items.

Challenges persisted at the other end of the income spectrum, where lingering inflation and dwindling pandemic savings weigh on household budgets. Etsy noted that lower-income households underperformed relative to higher-income households. eBay, which saw strength in luxury handbags and collectables, seconded that point.

Tariffs were a new theme. While how this ends up is anyone’s guess (sorry, Canada?), companies like Etsy and ThredUp with limited exposure to China made sure to get that point out. With trade policy if flux, this is another area giving managers heartburn.

Deep Pocketed, But Frugal

After working off the pandemic hangover, e-commerce is back to investing in growth in 2025. Thankfully, the tenor here is more sober. The focus now is on marrying growth with operational discipline, as opposed to the swashbuckling, growth-at-all-costs mentality during the ZIRP era.

Companies got religion around expense management in 2022 and 2023 and it’s sticking. Shopify is the poster child. In 2024, it grew sales 26% while reducing headcount from 8,300 to 8,100. That’s textbook operating leverage. In 2025, Shopify plans to grow revenue over 20%, while keeping headcount flat. The company is selectively investing. Here’s CFO Jeff Hoffmeister:

It is important to note that while we've significantly expanded our free cash flow margins over the last two years, as we move into 2025, and as I mentioned on our last call, we believe the free cash flow margin profile that we have achieved in 2024 strikes the right balance between profitability and investing in building the best products for our merchants today and into the future. We aim to maintain this level of cash flow profitability rather than optimizing for further margin expansion in the near term. There are simply too many compelling growth opportunities ahead.

Since 2020, Shopify has tripled revenue and grown operating income by twelve times, so it’s earned the right to maintain margins in 2025.

Amazon is in the same camp. While it plans to spend $100 billion on capital expenditures in 2025–largely in AWS to support insatiable AI demand5–it is also turning over the couch cushions to look for pennies. (Good things happen when you count pennies.)

On a per unit basis, Amazon’s cost-to-serve fell in 2024 for the second consecutive year. It’s going for a hat trick in 2025. Management sees opportunities to reduce costs by redesigning inbound fulfillment, adopting robotics, improving inventory placement, and adding more same-day delivery capacities, which are both faster and cheaper6.

While the checks are smaller, eBay, The Real Real, and ThredUp are investing too. The latter hopes to accelerate revenue growth by investing in customer and supply acquisition, while holding margins flat year-over-year.

Strong growth buys a lot of goodwill. In contrast, Wayfair has less flexibility. With furniture sales slumping, the company’s CFO alluded to additional cost cutting in 20257:

So we think that through ongoing expense management, even with a challenging top line environment, we can continue to grow adjusted EBITDA dollars.

After exiting Germany in January, the company cut tech headcount by over 10% and shut its tech hub in Austin, Texas in early March8. Since 2022, Wayfair has conducted five rounds of layoffs. It has been more aggressive than most on this front due to its high exposure to moribund home and living category as well as a rickety balance sheet.

Relative to peers, Etsy has been timid in cutting costs. With Elliott Management on the board, you have to think that will change in 2025 if growth prospects don’t improve.

AI

It wouldn’t be 2025 if I didn’t mention AI, so where we go. AI remains an investment area with AI and ML engineers scorching hot commodities in a slowing tech labor market. While the technology has yet to transform P&Ls–and possibly never will–AI data points were peppered throughout prepared remarks. For example, over 10 million eBay sellers have used the company’s Magical Listing tool to create over 100 million listings. ThredUp had over 1.3 million image searches in 2024 and these saw 85% conversion uplift. The RealReal reduced inbound processing time by one day, increasing throughput and reducing costs9.

None of these initiatives are needle moving outright, but that’s alright. E-commerce is trench warfare; there are no silver bullets. You need lots and lots of lead: saving $0.02 per order here, boosting conversion by a basis point there. Little improvements compound over time. At minimum, the promise of generative AI is providing more foot soldiers.

The e-commerce landscape is shifting, but the playbook remains the same: drive efficiencies, expand moats, and invest strategically. Growth-at-all-costs is out; profitable, defensible expansion is in. AI is adding new tools to the arsenal, but this remains a war of attrition–where survival favors those with scale, discipline, and strong execution.

If you’re finding this content valuable, consider sharing it with friends or coworkers. ❤️

For more like this, consider subscribing. ❤️

More Good Reads and Listens

Past quarterly e-commerce reviews from Below the Line: Q3 2024 - Normal-ish, Q2 2024 - A Knife Fight In Mud, Q1 2024 – Keep It Simple, Q3 2023 – Back to Basics, Q2 2023 – Harvest Season, Q1 2023 – Nature is Healing, Q3 2022 – Naughty or Nice? (Part 1), Q3 2022 – Naughty or Nice? (Part 2), Q2 2022 – Slimming Down (Part 1), Q2 2022 – Slimming Down (Part 2), Q1 2022 – An E-commerce Recession (Part 1), Q1 2022 – An E-commerce Recession (Part 2).

Disclosure: The author owns shares of Shopify.

Unless otherwise noted, all growth rates are year-over-year.

Overall GMV growth was down 7% due to positive contributions from its M&A portfolio: Depop, a marketplace for second-hand fashion, and Reverb, a marketplace for used musical instruments.

The most generous interpretation here is that Etsy’s longer shipping times relative to someone like Amazon made it more vulnerable to fewer holiday shopping days. Still, The RealReal and ThredUp both saw growth accelerate and they hardly offer Amazon Prime-level shipping speeds.

Wayfair, Q4 2024 Earnings Call, February 20, 2022.

Amazon CEO Andy Jassey said that AI is the largest opportunity since the cloud.

For Amazon, faster delivery speeds are driving higher purchase frequency, especially for everyday essentials and pharmacy items. The company has seen no diminishing returns on ROI on faster delivery. More on that here.

Wayfair, Q4 2024 Earnings Call, February 20, 2022.

Wayfair form 8-k filed on March, 7, 2025.

Here’s more detail on how The RealReal plans to use AI to further reduce processing times:

In 2025, we are launching our Athena AI initiative, addressing the processes that happen from the time an item arrives in our authentication center to the time it's launched on our site. Athena leverages our data assets and AI capabilities to drive significant efficiencies. This enhancement aims to optimize our workflow and uses sophisticated image recognition to authenticate and pre-populate key item attributes. More accurate item attribution results in improved search, higher customer satisfaction, lower returns, better pricing accuracy, and quicker time to launch.