#153 - Misery Loves Company

Getir Acquires Gorillas

Hi 👋 - Over the past year, over 50% of instant delivery startups have failed or been acquired. Consolidation continued in December, with Getir buying European rival Gorillas. Below, a look at the deal and the challenges of running an instant delivery business. As always, thanks for reading.

🛍 If you’re finding this content valuable, consider sharing it with friends or coworkers.

🛍 For more like this once a week, consider subscribing.

Poof

Gorillas wasn’t cut out for magic. While a magician never reveals his secrets, Gorillas showed everyone how to make $1 billion disappear: by starting an instant grocery delivery company.

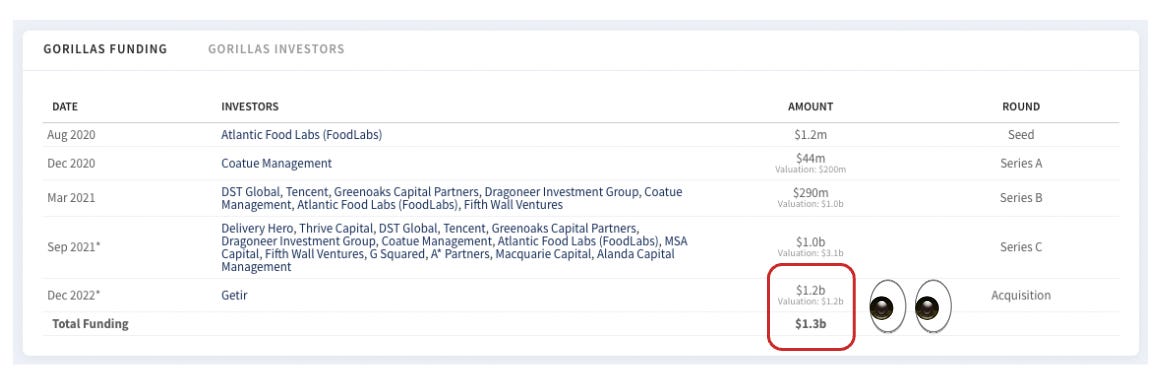

Founded in May 2020, the Berlin-based business achieved unicorn status in under a year, a record for German start-ups1. Its decline was equally quick. Having raised $1.3 billion, it was acquired by Getir in December 2022 for $1.2 billion, after incinerating most of its cash.

According to the Financial Times, the deal valued Gorillas at $1.2 billion and the combined entity at $10 billion. This represents a 60% haircut from Gorillas’ September 2021 valuation of $3.1 billion and a 15% discount from Getir’s March 2022 valuation of $11.8 billion (or roughly 30% when backing out Gorillas). That seems skimpy compared to public market comps like Delivery Hero, DoorDash, and Uber who shed 40-60% of their market cap over the past year, or Instacart, which slashed its private valuation by 75%.

Burn Baby Burn

Like Getir, Gopuff, and Jokr, Gorillas provides speedy delivery of groceries and convenience items. Like Getir, Gopuff, and Jokr, Gorillas caters to cash-rich, time-starved urbanites. Like Getir, Gopuff, and Jokr, Gorillas operates a network of micro-fulfillment centers (MFCs) serving nearby neighborhoods. You get the point. Aside from the color of the delivery driver’s uniform – Gorillas is black, Getir is purple and yellow – and where they operate, there’s not much differentiation between instant delivery business models.

Another trait these models share is burning boatloads of cash. According to Bill Gates:

The first rule of any technology used in a business is that automation applied to an efficient operation will magnify the efficiency. The second is that automation applied to an inefficient operation will magnify the inefficiency.

Here’s a corollary: the first rule of unit economics is that scaling a business with positive unit economics builds value. The second rule of unit economics is that scaling a business with negative unit economics destroys value. Wal-Mart typifies the first rule. For years it was unprofitable as it aggressively expanded its store count, but the unit economics of the individual stores was rock solid. Gorillas is a case study in the second rule – burn intensified as it scaled.

The company’s cash flow statement makes the Earth Liberation Front look like Smokey the Bear. According to the Financial Times, Gorillas2:

Spent €8 per order on marketing during the first half of 2022. For context, average order values are probably in the €30-€50 range and gross margins are likely in the 40% range. That doesn’t leave much to cover logistics, operations, technology, and other overhead.

Burned over €750 million in the year ending July 31, 2022, averaging over €60 million per month.

Lost €1.50 for every €1 of revenue3.

Nothing focuses the mind like a rapidly dwindling cash balance and no access to capital. (Gorillas tried unsuccessfully to raise more cash in late 2022.) To stem the bleeding, the company pivoted from hyper-growth to establishing a path to profitability in May 2022. This included laying off 300 employees, about half of its global office staff, and exiting underperforming markets like Belgium, Denmark, Italy, and Spain. (Getir also conducted a 14% layoff in May 2022.) But it was too late to apply a tourniquet. Ultimately, Gorillas burned through most of the $1.3 billion it raised4. In a move reminiscent of MissFresh, it even stopped paying some suppliers5. Its alternatives were bleak: find a buyer or go belly up. Things were so tight that Gorillas had to take out a loan to keep the lights on while Getir completed its due diligence6.

What Getir Gets

Getir threw Gorillas a lifeline for a few reasons. One strategic rationale for the acquisition was Gorillas’ network of 140 MFCs spread across 44 cities7. About 90% of Gorillas’ revenue comes from its top five markets: France, Germany, the Netherlands, the UK, and the US8. Getir operates in all of these markets, and the two companies have considerable overlap in cities like Amsterdam, Berlin, London, and Paris.

The critical metric for instant delivery is the number of drops per hour. The higher, the better. Demand is the limiting factor. By consolidating, Getir can improve this metric in neighborhoods where it overlaps with Gorillas by aggregating demand. This should increase route density and potentially enable batching. Today, both companies's MFCs are operating well below capacity. Aggregating demand will increase MFC volume and utilization rates. For this to play out, Getir needs to close redundant MFCs in areas where Gorillas and Getir serve the same neighborhood.

There’s a regulatory angle as well. In the Netherlands, Amsterdam, Rotterdam, and Utrecht have put a one-year moratorium on opening MFCs. Similarly, Paris, where Gorillas has a solid footprint due to its acquisition of Fritchi in early 2022, is cracking down on new MFCs9. The acquisition expands Getir’s footprint in markets that would have been difficult to enter organically.

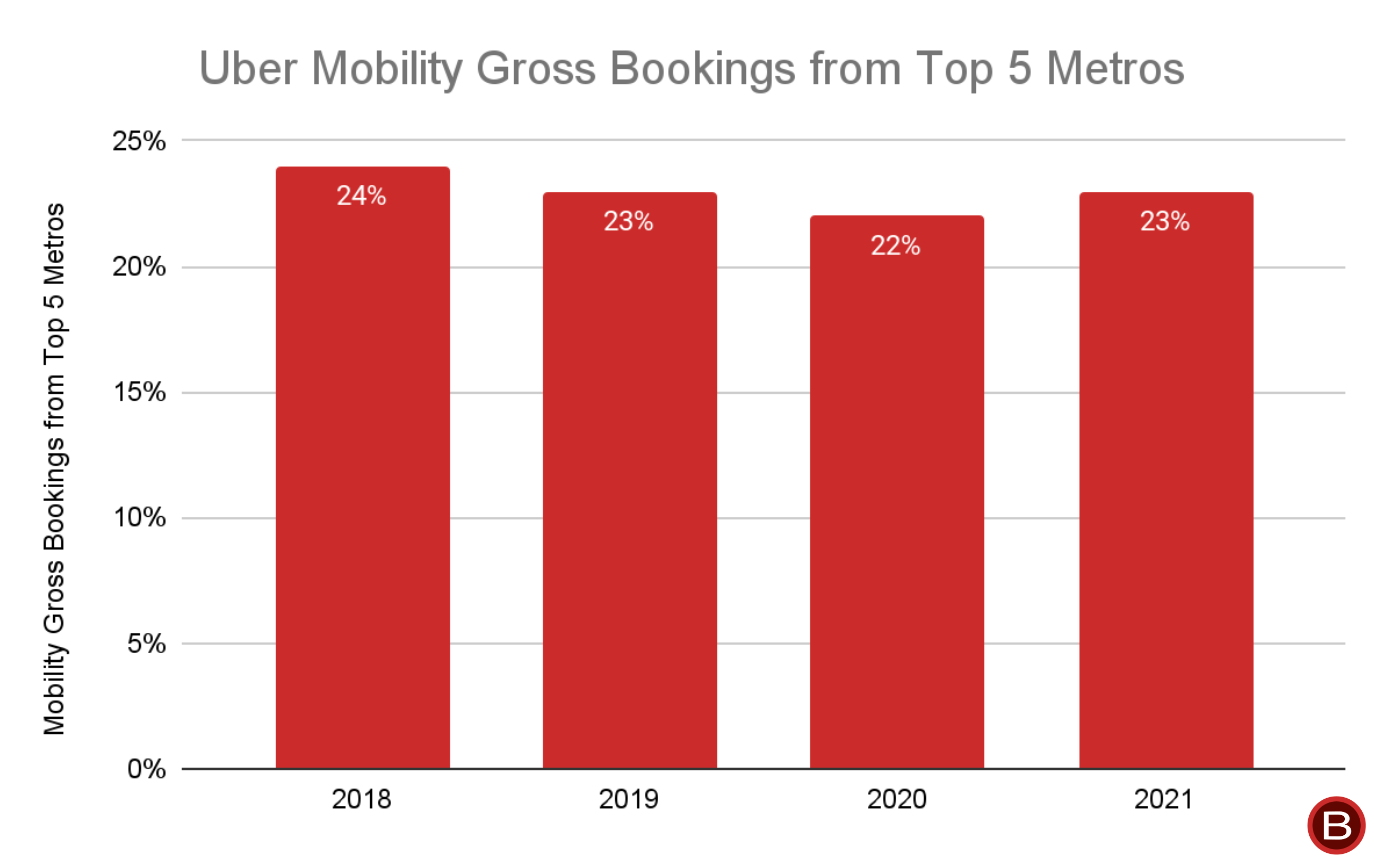

Given power law dynamics, a few cities can generate a disproportionate volume of sales. For example, Uber operates in thousands of markets, but about 25% of its revenue comes from its top five cities. If instant grocery delivery is similar to ride hailing in this respect, having a strong footprint in markets like Paris and London is a plus.

The deal could also lower Getir’s customer acquisition cost (CAC). Over the past two years, nearly two dozen VC-backed instant delivery firms have been knife-fighting for customers. Not all operate in the same markets, but in cities like London, New York, or Paris there’s intense competition. That’s expensive. To date, the biggest winners from instant delivery are Facebook, Google, Twitter and customers who get free ice cream. Having one fewer bidder in ad auctions could decrease CAC. When a consumer internet start-up dies, CAC often has its fingerprints all over the crime scene, so this is a win.

It also expands Getir’s customer base, potentially allowing it to lean more into retention for growth (as opposed to acquisition). This will be an uphill battle. According to Quartz, Getir, Gopuff, and Gorillas discounted a substantial percentage of orders – over 80% in some months – in France and the UK in 2022. This is one of the reasons why Gorillas spent €8 on marketing per order. To woo customers, instant delivery firms spend fortunes on promo codes and aggressive discounts. What’s been reported about the industry suggests turning off the tap is difficult.

Lastly, the best time to buy is when someone is forced to sell. Gorillas was a forced seller. Their alternative to a deal was bankruptcy. Getir was savvy on this front. To be opportunistic, a company needs cash or access to financing. In March 2022, Getir raised $800 million making it one of the industry’s best capitalized players right before capital markets went south. While the Gorillas deal was mostly equity, the cash infusion gave Getir the confidence to pull the trigger.

Nazim Salur, Getir’s CEO, believes that instant delivery will play out like the grocery industry, with two or three major players dominating each market. His goal is to be one of the last companies standing10. Consolidation is part of his playbook. For example, in November 2021, Getir acquired UK-based Weezy. With Gorillas taken out of its misery, the European instant delivery market is now a two man race between Getir and Flink, a Berlin-based competitor backed by DoorDash. (That’s probably still two too many.)

Mountain or Trash Heap?

A consolidating market and limited access to capital advantages larger players with cash on their balance sheets. As such, Getir and Gopuff are well positioned to be the industry’s last survivors. Yet that might be a pyrrhic victory. First, DoorDash, Lyft, and Uber have shown that consolidation is no panacea for profitability. Second, it’s unclear if anyone in the industry has cracked the unit economic puzzle. Grocery is a low margin business, dependent on scale and operational efficiency. Delivery is a low margin business, dependent on scale and operational efficiency. Combining the two doesn't make operating easier. The risk for Salur is that he fights his way to the mountaintop, only to find out it’s a trash heap.

Whenever I think about instant delivery, I think of Warren Buffett's quote:

When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.

Instant delivery is a business with a reputation for bad economics. Delivery is a game of inches and seconds, with little margin for error. It’s capital intensive, competitive, manual, and has high variable costs, limiting the scope for fixed cost leverage. Although none of the companies are public, making the financial picture incomplete, reporting from the Financial Times, The Wall Street Journal, and Quartz paints a dismal picture. About half of the instant delivery start-ups operating in 2021 folded by the summer of 202211, a mortality rate on par with Ebola. To be fair, most start-ups fail and most industries consolidate with time – instant delivery start-ups just seem to be doing this on an accelerated timeline.

At $10 billion, Getir is valued like a tech company. But it isn’t a tech company. It delivers groceries. According to Ben Thompson, the question of whether a company is a tech company is determined to the extent its business model is governed by software’s unique characteristics. I reference this framework frequently because it’s a good checklist. And checklists help avoid mistakes. Ask a pilot.

Does Getir create ecosystems? No. Lol.

Does Getir have zero marginal costs? No. Toilet paper isn’t free. Neither is delivery. In addition to hefty delivery expenses, the cost of goods sold are 50-70% of order value12.

Does Getir improve over time? Maybe. Better merchandising and personalization could improve the user experience over time. However, the guts of the business – delivery bikes, MFCs – are subject to wear and tear and depreciation. Maintenance capex requirements are likely to be material.

Does Getir offer infinite leverage? No. While there’s room for operating leverage on tech infrastructure, there are high marginal costs for delivery. Atoms are harder than bits. Due to the laws of physics, traffic safety rules, and Murphy’s Law (another seventh floor walk-up?!) there are limitations to the number of orders that can be delivered per hour. Four deliveries per hour seems like an upper limit.

Does Getir enable zero transaction costs? No. There are substantial customer acquisition costs with limited retention.

A central limitation of these business models is that marginal costs are so high that the number of orders needed to cover fixed costs are enormous. To make it work, you’d need modest CAC, healthy retention, and lean overhead, three characteristics the industry lacks.

Paging David Copperfield

From my view in the cheap seats, there’s a lot up in the air, and plenty of reason for skepticism. It’s unclear if consumers want this service enough to pay full freight for it. It’s unclear that if they do, it’s a viable model outside a handful of neighborhoods in a handful of cities. While “everyone eats” equates to a big TAM in a pitch deck, industry performance suggests limited appetite for these services. It’s also unclear why Getir should keep its high-growth SaaS company multiple, and not be valued like a grocer (if it ever IPOs, I suspect the public markets will correct this). Getir is in a better position today than before it acquired Gorillas, but combining two bologna sandwiches doesn’t create prime rib. That’s a magic trick that even David Copperfield couldn’t pull off.

🛍 If you’re finding this content valuable, consider sharing it with friends or coworkers.

🛍 For more like this once a week, consider subscribing.

More Good Reads and Listens

Quartz on why nobody wants to pay for instant grocery delivery. The Financial Times why investors are souring on the space. Sam Altman on unit economics. Below the Line on Getir’s business model and Misfits Market’s acquisition of Imperfect Foods.

Disclosure: The author owns shares in Alphabet.

Financial Times, Most rapid grocery apps fail to deliver for investors, October 14, 2022.

Financial Times, Most rapid grocery apps fail to deliver for investors, October 14, 2022.

The Financial Times, Getir acquires grocery app rival Gorillas in $1.2bn deal, December 9, 2022.

Financial Times, Most rapid grocery apps fail to deliver for investors, October 14, 2022.

Sifted, The real reason Getir wants to buy Gorillas?, November 25, 2022.

The Financial Times, Getir acquires grocery app rival Gorillas in $1.2bn deal, December 9, 2022.

Sifted, The real reason Getir wants to buy Gorillas?, November 25, 2022.

Gorillas, Gorillas Announces Internal Changes, May 24, 2022.

Sifted, The real reason Getir wants to buy Gorillas?, November 25, 2022.

Financial Times, Most rapid grocery apps fail to deliver for investors, October 14, 2022.

This is a best guess, based on companies admittedly scarce disclosures. Based on podcasts with executives, GoPuff has gross margins in the “high-forties.” Jokr’s long-term model calls for gross margins of 40% (equating to a 60% cost of goods sold). They’d be lower today as Jokr isn’t operating anywhere near its long-term model. According to reporting by The Wall Street Journal, now defunct Fridge No More had an average basket size of $33 and cost of goods sold of $22.10, equating to roughly 33% gross margins.